2025 ACTUARIAL RECRUITING REVIEW

Looking back on 2025, the U.S. job market delivered modest growth, with approximately 700,000 net job gains over the year. While hiring activity varied by industry, overall employment conditions for actuaries remained steady as employers balanced economic uncertainty with continued demand for specialized skills.

In 2025, the actuarial job market stood out for its stability. Actuarial unemployment remained under 1% throughout 2025, underscoring the continued and growing need for actuarial expertise across all insurance areas. Demand was driven largely by organizations’ increasing focus on risk management, and the need to replace actuaries retiring or leaving the industry. While many new roles are expected to be growth-driven, replacement hiring also remains important as experienced actuaries retire or transition out of the field.

Long-term growth projections further reinforce the strength of the profession. According to the U.S. Bureau of Labor Statistics, employment of actuaries is projected to grow 22% from 2023 to 2033—far outpacing the 4% projected growth rate for all occupations.

The insurance sector continued to be a primary engine of actuarial hiring in 2025, as carriers expanded into new markets and invested in advanced analytics to evaluate increasingly complex risks. Property and casualty roles remained strong, while health insurance, life insurance and pensions experienced more moderate hiring. In addition, actuaries with expertise in cybersecurity risk and ESG (Environmental, Social, and Governance) considerations were sought after, reflecting evolving risk priorities across industries.

Overall, 2025 reinforced actuaries’ reputation for job security and career resilience. The profession continued to rank highly across multiple categories—including top business jobs, top STEM jobs, top-paying jobs, and “Best Jobs Overall” —as recognized by U.S. News & World Report. As the year concluded, actuarial science remained one of the most attractive and future-proof career paths in the U.S. labor market.

2026 U.S. ACTUARIAL MARKET OUTLOOK

Strong growth prospects continue for the actuarial market in 2026, outpacing the average across all occupations. This reflects the expanding demand for actuaries who can assess and manage risk in insurance, healthcare, finance, and enterprise risk functions.

- The U.S. Bureau of Labor Statistics projects roughly 2,400 openings per year on average through the mid-2030s, including growth positions and replacements due to retirements and career changes.

- Actuarial job growth should remain significantly above the 3–4% average for all occupations in the U.S.

The actuarial profession historically exhibits an exceptionally low unemployment rate, typically under 1%, due to specialized skill sets and ongoing demand across multiple sectors. Even as the U.S. labor market showed slower job gains and a moderate unemployment rate (~4.4%) in late 2025, this has not significantly softened the demand for actuarial talent. Historically, as niche analytical professionals, actuaries are not subject to general economic cycles in the same way as broader occupations. Insurance carriers, especially in property/casualty, life, and health insurance, continue to signal the need for actuaries with advanced modeling, pricing, and risk evaluation skills. In addition, enterprise risk management and regulatory requirements (e.g., evolving solvency and reporting standards) also fuel actuarial hiring. Evolving needs for 2026 include cybersecurity risk modeling, climate risk assessments, and healthcare cost modeling.

As the modernization of actuarial work accelerates in 2026, a growing share of actuarial tasks are being powered by automation, data engineering, and machine learning frameworks. These trends indicate that actuaries in 2026 must combine traditional probability and statistics with data engineering, analytics, and technology governance skills to add value beyond routine analysis.

While compensation can vary by experience, certification level, and industry, actuaries remain comparatively well-paid professionals in the STEM and financial risk sectors. Actuarial careers continue to be recognized among the top jobs in the United States based on job stability, pay, and prospects, according to U.S. News & World Report rankings through 2025.

Here are the major trends that are expected to shape the actuarial job market this year:

- Specialization – Actuaries with advanced modeling, machine learning, and risk governance expertise are in highest demand.

- Knowledge of AI/GenAI, cloud platforms, and data pipelines will differentiate candidates.

- AI and automation tools will not be replacing actuaries, but will be automating routine reporting functions

- AI tools will shift actuaries away from repetitive tasks and towards strategic and advisory roles

- General U.S. job gains slowed in 2025, but actuarial hiring should remain steady due to specialized needs in the insurance industry.

- Traditional sectors (life, health, property/casualty) will still drive the bulk of actuarial roles.

- Non-traditional roles will grow, with enterprise risk and analytics functions increasingly employing actuaries outside pure insurance contexts.

RETURN TO OFFICE

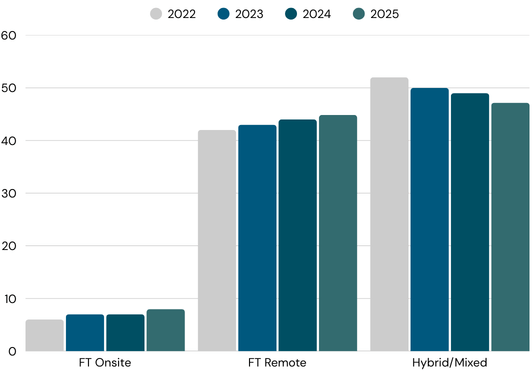

By 2026, employers’ approach to return to office (RTO), hybrid, and remote work has evolved significantly compared with the past few years. After the pandemic, companies initially rushed to adopt fully remote models in 2020–2022, but over the past three years employers have gradually shifted toward bringing employees back onsite, usually in a structured hybrid arrangement. Most actuarial employers are now requiring employees to be in the office a set number of days per week. Hybrid work has emerged as the dominant model, with hybrid roles accounting for a growing share of job postings and fully remote roles remaining a smaller but important segment of the labor market.

Fully remote work has declined dramatically from its pandemic highs, and only about 10 % of U.S. job postings in 2025 were fully remote, even as hybrid opportunities continued to expand. Employees clearly value flexibility, with many saying they would look for new jobs if hybrid or remote options were revoked. Actuarial candidates rank hybrid work among their top priorities in job searches.

In the last 2 years employers have been tightening office requirements, with some large companies requiring four or five in-office days per week for certain roles or offering voluntary exit packages to employees unwilling to comply. This reflects a belief among some executives that face-to-face collaboration enhances productivity, creativity, and culture. At the same time, data indicates that hybrid remains the most widespread and stable model with most companies continuing to offer flexibility rather than returning fully to on-site work, and hybrid arrangements now form the default for many organizations. Employers are also increasingly refining RTO policies to tie in-office days to specific goals, rather than mandating attendance without context.

INDUSTRY TRENDS FOR 2026

LIFE INSURANCE

The life insurance market is entering a period of adjustment driven by economic conditions, changing customer needs, and ongoing regulatory developments. Higher interest rates have generally improved investment income for insurers, supporting earnings and pricing flexibility. At the same time, market volatility has increased, requiring insurers to be more cautious in how they manage their investments and long-term obligations.

Product offerings are continuing to evolve in response to both consumer preferences and financial considerations. Insurers are placing greater emphasis on products that offer flexibility and lower long-term risk, such as policies tied to market indicators or focused primarily on protection rather than savings. This shift reflects a desire to balance customer value with financial stability, while also responding to increased competition and the demand for more customizable solutions.

Trends in mortality and longevity remain an important area of focus. While death rates have improved compared to the height of the pandemic, they have not fully returned to long-term historical patterns and vary across different population groups. Insurers are closely monitoring these trends, particularly as medical advances and lifestyle changes continue to influence life expectancy.

Insurers are facing greater expectations around transparency, risk management, and financial resilience, from both regulators and rating agencies. As a result, companies are investing more in stress testing, governance, and long-term planning to ensure they can meet their commitments to policyholders under a wide range of economic conditions.

Looking ahead, technology and data will play an increasingly important role in the life insurance market. Insurers are using improved analytics and digital tools to make faster, better-informed decisions, enhance customer experiences, and manage risk more effectively. Faster, more streamlined digital application/underwriting, thanks to technology adoption and the resulting shorter waiting times, easier online purchasing, and more personalized pricing means that success in this environment will depend on an insurer’s ability to adapt to change and maintain trust with policyholders.

In 2026 we can expect a growing availability of hybrid products which include savings, long term care or investment components. More streamlined digital applications will make personalized pricing, and easier online purchasing, the norm.

ANNUITIES

The annuities market is expected to remain strong as higher interest rates continue to make income-oriented products more attractive to consumers. Improved yields allow insurers to offer more competitive payout rates, which has driven an increase in demand from retirees seeking predictable income and protection from market volatility. While this environment supports growth, it also requires insurers to carefully manage investment risk and ensure they can sustain promised benefits over time.

Product innovation in the annuities market is focused on balancing growth potential with risk management. Fixed and fixed indexed annuities remain, while registered index-linked annuities continue to gain traction among customers willing to accept some market risk in exchange for higher return potential. Retail annuity sales in 2025 consistently exceeded $120 billion per quarter. In 2026 historically high sales are expected, with an aging population sustaining long-term demand. These trends reflect a shift toward offering customizable solutions that can adapt to different retirement needs and risk tolerances.

Longevity risk remains a central consideration for annuity providers. As people continue to live longer on average, insurers must ensure that lifetime income products are designed and priced to remain sustainable over extended payout periods. At the same time, retirement behavior is becoming more varied, with policyholders delaying or accelerating withdrawals based on market conditions and personal circumstances. Monitoring these behavior patterns is critical to managing long-term obligations.

Insurers face heightened scrutiny around reserve adequacy, capital strength, and the use of reinsurance and asset structures. Regulators and rating agencies are emphasizing stress testing and transparency, which is encouraging insurers to strengthen governance and risk management practices while maintaining competitive offerings.

Looking ahead, demographic trends and technology will play a key role in shaping the annuities market. An aging population and growing need for retirement income solutions provide a strong long-term demand outlook. There will potentially be more interest in annuities and retirement products as insurers market more customized products as part of a long-term savings and retirement plan. As advances in data, analytics, and digital distribution enable insurers to better understand customer needs, streamline operations, and design more effective retirement income products, success will depend on aligning innovation with financial discipline and maintaining consumer confidence.

HEALTH

The health insurance market in 2026 is expected to remain under pressure from rising medical costs, shifting utilization patterns, and continued policy uncertainty. Healthcare inflation is projected to stay elevated, driven by higher prices for hospital services, prescription drugs, and specialty care, as well as increased use of services following deferred care in prior years. Employer healthcare costs are estimated to rise by 8.5%-9.5% in 2026. For insurers, this creates an environment where premium affordability and cost control will be significant challenges for employer-sponsored and individual market plans. A key concern in 2026 is the expiration of the Affordable Care Act (ACA) premium tax credits at the end of 2025. As of this writing, the policy remains uncertain. Without these subsidies many consumers face dramatically higher premiums, contributing to enrollment volatility.

Consumer behavior continues to evolve as virtual care, outpatient services, and value-based care arrangements are becoming more common. Utilization of services is expected to grow as the population ages and as awareness and diagnosis of chronic conditions increase. Health insurers are increasingly focused on managing total cost of care through network design, care coordination, and partnerships with providers. As insurers adopt AI and automations, there is potential for more efficient claims processing, fraud detection, and personalized plans. This may help stabilize costs and improve customer experience.

Government programs will remain a major driver of health insurance growth and complexity. Medicare Advantage enrollment is expected to continue expanding, supported by an aging population and consumer interest in supplemental benefits and integrated care models. Medicaid enrollment may stabilize or decline slightly following recent eligibility changes, but it will remain a significant and closely monitored segment. Ongoing changes to reimbursement rules, risk adjustment, and quality programs will require insurers to stay agile and responsive. The rising use of expensive treatments (including weight loss drugs), behavioral health demands, the cost of chronic conditions, and expensive new prescription drugs will be concerns for the long-term sustainability of payers and insurers.

Regulatory and political changes will continue to influence the market in 2026. Health insurers face heightened scrutiny around premium increases, benefit design, and access to care, alongside growing expectations for transparency and consumer protection. Policy debates around drug pricing, mental health coverage, and preventive care are likely to shape future requirements, adding uncertainty to long-term planning and pricing strategies. Premium increases may lead to individuals reconsidering coverage, particularly those who consider themselves to be healthy.

Looking ahead, data and technology will play an increasingly important role in managing risk and improving outcomes. Health insurers are investing in analytics, artificial intelligence, and digital tools to better predict costs, identify high-risk members, and support proactive care management. Health insurance is increasingly focused on managing uncertainty in enrollment, regulatory policy and pharmacy costs. Success in the 2026 health insurance market will depend on balancing affordability, quality, and financial sustainability while building and maintaining trust with members, providers, and regulators in an evolving environment.

PROPERTY & CASUALTY

The property and casualty (P&C) insurance market in 2026 is expected to remain challenged by elevated loss costs, ongoing catastrophe risk, and continued economic uncertainty. While premium rate increases over recent years have helped restore profitability in some lines, inflation in repair costs, labor, and litigation continues to pressure results. Rating agencies like Fitch Ratings are expecting the industry to remain profitable and stable, but with less momentum than in 2025.

Natural catastrophe exposure will remain a defining feature of the P&C market. More frequent and severe weather events, including hurricanes, wildfires, and convective storms, are driving higher volatility and increasing the cost of reinsurance. In response, insurers are ensuring that product offerings are appropriately priced for regional risk. These dynamics are leading to reduced capacity or tighter underwriting in high-risk areas, particularly in personal property lines.

Casualty lines such as personal and commercial auto and general liability are seeing higher jury awards (nuclear verdicts), expanded liability theories, and increased litigation funding, which are contributing to rising claims and longer settlement timelines. Insurers are responding with higher rates, tighter underwriting standards, and increased use of data and analytics to better assess risk and manage claims outcomes. Personal auto is a key driver of profitability and a battleground for customer acquisition. Homeowners insurance has stabilized, but affordability remains a concern, particularly in areas prone to severe weather.

Regulatory and capital considerations will also shape the P&C landscape in 2026. Regulators are closely scrutinizing rate filings, market availability, and insurer solvency, particularly in catastrophe-prone states. At the same time, reinsurance capacity and pricing remain key considerations for capital management, influencing risk appetite, portfolio mix, and growth strategies across the industry.

Looking ahead, technology and analytics will play a growing role, with insurers investing in advanced catastrophe modeling, telematics, and automated claims handling to better price risk, control costs, and enhance customer experience. 2026 is expected to see Ai move from experimental to operational scale, embedding AI into underwriting, pricing, claims automation and risk selection. Success in this year’s P&C market will depend on disciplined underwriting, effective capital and reinsurance strategies, and the ability to adapt to a more volatile and complex risk environment.

LIFE & ANNUITIES REINSURANCE

The U.S. life and annuities reinsurance market in 2026 is expected to remain active and strategically important as insurers continue to manage capital, earnings volatility, and balance-sheet risk. Demand for reinsurance is being supported by higher interest rates, which have improved the economics of certain transactions. At the same time, reinsurers are maintaining disciplined pricing and underwriting standards, reflecting a more cautious approach to long-term risk taking. The structure of reinsurance transactions continues to evolve, and regulators and rating agencies are paying closer attention to these arrangements, increasing the emphasis on transparency and governance.

Market capacity in 2026 is expected to remain sufficient but concentrated among a smaller number of well-capitalized global reinsurers, favoring long-term relationships, stability, execution certainty, and strategic support.

Looking ahead, the U.S. life and annuities reinsurance market will continue to be shaped by demographic trends, regulatory oversight, and advances in data and modeling. As insurers face growing complexity in product design and risk management, reinsurance will remain a critical tool for maintaining financial strength and flexibility. Success for both insurers and reinsurers in 2026 will depend on disciplined risk selection, strong governance, and the ability to adapt to evolving market and regulatory expectations.

P&C REINSURANCE

The U.S. P&C reinsurance market in 2026 is expected to remain firm, shaped by elevated catastrophe losses, economic uncertainty, and heightened risk awareness across the industry. While recent years of rate increases have improved reinsurer profitability, loss volatility from severe weather events continues to drive a cautious underwriting environment. Reinsurers are entering 2026 prioritizing sustainable returns over rapid growth.

Catastrophe risk remains the dominant driver of demand for P&C reinsurance. More frequent and severe hurricanes, wildfires, floods, and storms have increased insurers’ reliance on reinsurance to manage exposures and protect capital. In response, reinsurers continue to push for tighter terms, particularly in catastrophe-prone regions.

Casualty reinsurance conditions are also expected to remain challenging. Claim costs are rising faster than general economic inflation due to societal shifts, including increased litigation, bigger jury awards (like nuclear verdicts), plaintiff-friendly legal trends, and greater public distrust in corporations. This leads to higher premiums and less coverage, and reinsurers being more cautious in assuming casualty risk. As a result, insurers may face higher costs or reduced availability for casualty reinsurance.

Capital considerations and alternative reinsurance capacity will continue to influence market conditions in 2026. While traditional reinsurers remain well-capitalized, alternative capital such as insurance-linked securities has become more selective, particularly for peak catastrophe risk. This has reduced overall capacity at lower price points and increased the value of stable, long-term reinsurance relationships.

Looking ahead, analytics and modeling will play an even greater role in the U.S. P&C reinsurance market. Advances in catastrophe modeling, climate analytics, and portfolio management tools are improving risk selection and pricing accuracy. P&C reinsurance in 2026 will depend on disciplined underwriting, strong capital management, and close collaboration between insurers and reinsurers in navigating a complex risk environment.

INSURTECH

The insurtech market in 2026 is expected to be more selective, following several years of recalibration after rapid growth and investment. While funding levels are likely to remain below prior peaks, capital is increasingly being directed toward companies with proven business models, and clear paths to profitability. The focus has shifted from disruption to practical solutions that deliver savings and better customer outcomes. Solutions focused on artificial intelligence, automation, and advanced analytics are gaining traction, particularly where they can reduce expense ratios, improve fraud detection, or enhance decision-making speed and consistency.

Regulatory scrutiny and governance expectations are increasing as insurtech solutions become more embedded in insurance operations. Insurers and regulators are paying closer attention to data privacy, model transparency, and the use of artificial intelligence in decision-making. Successful companies will be those that align closely with insurers’ strategic priorities, integrate seamlessly with legacy systems, and deliver clear improvements in efficiency, risk management, or customer satisfaction. Rather than reshaping the industry overnight, insurtech is becoming a steady driver of incremental change across the insurance industry.

CASTASTROPHE

The catastrophe insurance market in 2026 is expected to remain under pressure as the frequency and severity of natural disasters continue to rise. Hurricanes, wildfires, floods, and severe storms are driving higher loss volatility. While recent premium increases have helped strengthen insurer and reinsurer balance sheets, catastrophe risk remains one of the most complex areas of the insurance market.

Insurers are increasingly selective in the risks they underwrite, with higher deductibles, reduced limits, and more restrictive coverage terms becoming common. In some areas, limited availability of private insurance has increased reliance on public-private solutions, highlighting ongoing concerns around affordability and access to coverage for catastrophe-exposed properties.

Reinsurance and alternative risk transfer continue to play a critical role in supporting the catastrophe insurance market. Traditional reinsurance capacity remains disciplined, while alternative capital, such as catastrophe bonds and insurance-linked securities, is focused on well-modeled risks. These structures continue to be essential tools, though their cost and availability can fluctuate significantly following large loss years.

Looking ahead, the long-term sustainability of the catastrophe insurance market will depend on continued innovation and collaboration across the industry. Improved risk mitigation, resilient construction standards, and closer coordination between insurers, reinsurers, governments, and communities is essential. Success in 2026 will require a willingness to adapt to a risk environment that is evolving faster than ever before.

2026 RECRUITING OUTLOOK FOR ACTUARIES

CANDIDATES

The recruiting outlook for actuarial candidates in 2026 is positive, with strong long-term demand driven by increasing risk complexity across insurance, finance, healthcare, climate risk, and areas such as cybersecurity and enterprise risk management. Employment growth for actuaries continues to outpace the average for most professions, but hiring has become more selective as employers raise expectations around skills, experience, and specialization.

While traditional insurance roles in life, annuity, and property-casualty remain core hiring areas, organizations are increasingly seeking actuaries who can operate beyond pure modeling. In 2026, candidates who combine actuarial fundamentals with data analytics, programming (such as Python, R, or SQL), automation, and an understanding of AI or model governance are significantly more competitive. Many actuarial functions are modernizing, creating demand for hybrid roles that blend actuarial expertise with technology, business strategy, and risk oversight.

Entry-level hiring remains competitive. Employers often expect candidates to have passed at least two to three actuarial exams, completed internships, and demonstrated technical or analytical project experience. Candidates with only minimal exam progress may find it harder to differentiate themselves, especially when competing against peers who also bring data science or quantitative skills. In contrast, experienced actuaries continue to be in high demand.

Overall, the 2026 actuarial job market favors candidates who are adaptable. Organizations value actuaries who can communicate insights clearly, support strategic decision-making, and work effectively across business and technology teams. While economic uncertainty may cause some firms to be cautious in hiring, the need for skilled actuaries remains strong, especially for those who focus on exam progress, technical skills, and real-world experience.

EMPLOYERS

In 2026, actuarial employers are approaching hiring with a more strategic focus. Firms across insurance and consulting continue to see strong long-term demand for actuarial expertise, but they are increasingly selective about the skills and profiles they bring into their teams. Traditional insurance employers (life, annuity, property & casualty, and health) remain primary sources of demand, yet the character of that demand is changing. Companies want deeper specialization and are placing a premium on professionals who can blend traditional actuarial work with data analytics, AI/technical capability, and strategic business insight rather than just traditional pricing and reserving roles.

Across the industry, many employers are prioritizing candidates who go beyond core actuarial modeling to demonstrate programming skills (Python, R, SQL), familiarity with modern analytics and predictive techniques, and comfort with emerging technologies such as generative AI frameworks. These capabilities are increasingly viewed as essential because actuaries are now involved not just in calculating numbers, but in shaping data pipelines and integrating actuarial expertise into broader strategic decisions.

Employers also face ongoing competition for top talent and are recognizing that longer, drawn-out hiring processes can cost them candidates. Actuarial hiring teams must streamline interviews and decision-making to avoid losing talent to competitors. Hybrid and flexible work arrangements remain important in attracting candidates, even as some companies push for more office presence.

Another major shift for employers is the emphasis on career progression and culture. Offering competitive salaries alone is no longer enough to attract top talent, employers need to offer career development support, exam sponsorship, flexible work policies, inclusive benefits, and clear growth opportunities if they hope to differentiate themselves. This is particularly true for niche actuarial and hybrid analytical roles where candidates often field multiple offers.

Employers willing to invest in internal upskilling of actuaries to enhance technical and analytical expertise will succeed in hiring and retaining top talent. Efficient recruitment processes and competitive work-life offerings will also attract and retain top performers.

Download the full PDF report here.

DW Simpson has grown to become the largest actuarial recruitment firm because of our consistent results. We are constantly growing and evolving as recruiters and industry knowledge leaders, with an eye towards becoming more effective, better educated, and continuing to drive success for our clients and candidates. Because DW Simpson is highly specialized, we have the specific expertise required to provide our clients and candidates with the resources, advice and support they need in the actuarial field and other related analytics professions in the insurance industry. The actuarial recruitment and placement process is our specialty, and we do it better, faster, and more thoroughly than any of our competitors.